Whether you know it or not, you are probably investing in foreign currencies now. If you own an ETF or mutual fund in any international equity or fixed income product, you are taking a currency risk. It’s not an indirect risk; it’s as direct as it gets. Foreign holdings are priced in their native currencies, and every price movement is captured in the dollar denominated net asset value [NAV].

Even if you sell your foreign assets and invest only in American firms, you do not escape exposure. On average, large American firms do about 30% of their business in the international sphere. Their profits are immediately affected by movements in the currency markets. You can’t escape currency risks, but you can be aware of them, and you can do something to accommodate them.

The first line of defense against unhealthy currency risks is to make sure your portfolio is fully diversified in its international holdings. This spreads your currency exposure as widely as possible. Just as in stocks and bonds, where diversity is of utmost importance, the same applies to currencies and all other asset classes you own.

For many investors, just making sure your international holdings are well diversified is probably enough to reduce the currency risks to an acceptable level. But, you may want to add additional currencies to your portfolio, because there are substantial benefits derived from doing so. The most widely acknowledged benefit is the low correlation that currencies have with virtually all other classes. This feature of currenices is unique in its level of non-correlation. Other asset classes claim to be of low correlation (real estate, bonds, emerging markets for example), but when the correlations are quantified, currencies stand far above all others.

Just ask yourself, since early November of 2007 when equity markets began their slide, wouldn’t it have been great to have assets in your portfolio that actually increased in value over the period? Wouldn’t that help you keep on course for achieving your financial goals? It’s easy to talk “buy and hold,” but it isn’t so easy to actually stick to your guns when your investments drop by 20% or 30% in a steep market slide. This kind of market sends investors panicking to the sell window just when they should be standing fast.

Currency investing may provide just the cushion you need during rough periods, helping you to stay the course. And staying in the game is what it’s all about; you can’t win if you don’t play. If you panic and sell during the lowest periods, then you will be buying back at higher prices later - buying high and selling low - not what the doctor ordered.

If you decide to take a second step and buy currencies directly, you will discover some of the other properties of Forex (Foreign Exchange Currency) trading: first, currencies may actually make money for you by appreciating in price, and secondly, you will earn interest on your foreign currency holdings.

In Forex trading, a strategy that seeks to buy currencies that are expected to rise in price is called a “value strategy,” and it’s no different than your expectations that some equities are undervalued. If your analysis tells you that the Chinese Yuan, for example, is undervalued, then buy the Yuan. It’s available in an ETF (CYB) (from WisdomTree) or in an ETN (CNY) (from Van Eck/Morgan Stanley). If you are right, you’ll profit from the Yuan’s rise. If not, you will at least experience the second benefit from owning a foreign currency - you will earn interest on your investment. This comes about because the banks that hold the currency you bought use your investment deposit to purchase commercial and government-issued short-term interest bearing investments.

So, while you are technically holding currency, you are actually holding short-term debt obligations denominated in the currency you bought. When the debt instrument matures, the interest owed is paid and passed on to you. With the Yuan and most other emerging market currencies, where it’s often difficult to find local short-term deposit possibilities, the fund managers use futures contracts that accomplish roughly the same thing - you profit from receiving the differential between the spot price and the forward contract price. Either way, you earn something on your holdings.

This feature of earning interest on the currency you own is a significant strategy for making money on foreign exchange investments. It’s called the “carry trade,” and is responsible for trillions of dollars of currency trading. But, it is also possible you may incur a loss if the price of your currency falls during the time you were earning interest. This possibility makes holding foreign currencies different from holding U.S. dollars in a money market account. Money market funds are managed to keep a constant value - not difficult since there is no chance of the dollar falling in dollar value.

But when your money crosses an international border, the currency risk raises its head. This is a good reason not to engage in the carry trade - you might lose. Although currencies usually have lower volatility than equities, there are still risks. You must be comfortable that you want to take the risks and that you can afford the potential losses that may result from currency investing.

Once you have decided to allocate an appropriate amount to currencies in your portfolio, then the fun begins. Now you can choose among all the currencies available for trading, and the list is getting longer every month. This is a good thing, in my view, for not too long ago, if you wanted to hold Forex, you had to open a special trading account with one of the online trading brokers. It’s a fast-moving, wild and wooly environment, highly leveraged, where fortunes are made and lost on an hourly basis. This is not suitable for most investors, especially those who have lives outside the Forex arena.

Fortunately, a new kind of ETF and ETN has been recently introduced that allows an average individual investor to buy a fairly good range of currencies. There are currently about twelve pairs available, and additional pairs can be bought if you select one of the bundled exchange-traded products. Speaking of pairs, don’t be put-off by this terminology. In fact, one cannot speak of the dollar rising or falling without referencing another currency. The dollar can’t rise or fall in relation to itself; it can only change with respect to some other currency. Neither can any other currency. So, when you buy Mexican Pesos in the U.S., you are borrowing dollars from yourself and investing them in Pesos. You own a currency pair: U.S. Dollar/Mexican Peso. If you were in London and bought Pesos, your pair would be the Pound Sterling/Mexican Peso.

I’m going to post these lists in two groups: individual currency ETFs or ETNs, and bundled currencies of both formats.

Individual Currency Products:

Rydex Shares ETFs: Currencies: Australian Dollar (FXA), British Pound (FXB), Canadian Dollar (FXC), Euro (FXE), Japanese Yen (FXY), Mexican Peso (FXM), Swedish Krona (FXS) and Swiss Franc (FXF)

WisdomTree ETFs: Currencies: Euro (EU), Japanese Yen (JYF), Brazilian Real (BXF), Indian Rupee (ICN), New Zealand Dollar (BNZ), and South African Rand (SZR)

Barclays iPath ETNs: Currencies: Euro (EROS), British Pound (GBB), Japanese Yen (JYN)

Elements ETNs: Currencies: Australian Dollar (ADE), British Pound (EBG), Canadian Dollar (CUD), Euro (ERE), Swiss Franc (SZE)

Van Eck/Morgan Stanley ETNs: Currencies: Chinese Renminbi-Yuan (CNY), Indian Rupee (INR)

Bundled Currencies Product

PowerShares ETFs: Bundles: Group of 10 Carry Trade (DBV), U.S. Dollar UP (UUP), and U.S. Dollar Bearish (UDN)

Barclays ETNs: Barclays iPath Optimized Currency Carry (ICI), Barclays GEMS Index (JEM), Barclays Asian and Gulf Currency Revaluation Note (PGD).

In lieu of recommendations, let me leave you with disclosure on my current holdings: (BZF), (FXM), (JEM) and (UUP). If you will read through the currency posts I have made over the last year at Seeking Alpha, you will get a good idea of why I have chosen these products. But, I do not recommend others necessarily follow suit. My rationale is: the first two are individual carry trade holdings that pay high interest rates. The second two are bundles to give my portfolio more diversity and earn some interest; JEM holds fifteen emerging markets currencies and pays a good dividend. UUP holds the G10 currencies doubled up with leverage for the bullish dollar - strictly a value play.

I also keep tight limits on currencies as a percentage of my total portfolio. This year I have gradually allowed my allocation to be just under 15%. This is toward the high end of most recommendations. But this is a new area of investing, indeed, as all alternative asset classes are, and there is no consensus in the financial advisor community about it. Some don’t recommend any, some recommend more. Use your best judgment to keep the risks balanced and within your comfort zone.

You should support any decision you make with the full knowledge of the risks involved and a thorough investigation on your own about each possible investment. There are good reasons to own foreign currencies. There are also good reasons not to own them. Good luck!

All About eReading: News, Reviews,Opinion

Monday, September 22, 2008

Hard Times for Soft Currencies

August has been hard on emerging market currencies. Note the table below to see how much the currencies of some of the emerging markets fell last month.

*I put the PowerShares DB US Dollar Bullish Fund ETF (UUP) in the chart to show that part of the decline was due to the relative strength of the U.S. dollar.

There are two primary reasons for the battering these currencies took in August: economic slowdowns in America and Europe, and global inflation.

The slowdown in the developed economies affects emerging markets because they depend so much on exports. Investors fear it will get worse; if demand for finished products or commodities falls even a little, export-dependent economies will be hurt a lot. This describes most emerging markets today and accounts for much of the recent fall in the value of their currencies.

Unfortunately, the EM world has more than slowing demand to deal with. At the same time, that demand for their products is leveling off or falling, the tremendous growth in exports over the last few years has pushed wages and local prices up. This reaction has two unsettling effects: it encourages increased spending within the local economies, putting upward pressure on domestic prices, and it encourages businesses to raise prices to cover the higher labor costs. Combine these two factors with the increase in commodity prices that has spiked world-wide over the last few years, and you get a triple whammy of inflationary pressures.

The final result of this rather long chain of events is a tendency for local economies to raise interest rates in order to relieve inflationary pressure and ease the devaluation of their currency. Not every country does it this way, but, as you can see from the first table, many do.

Political instability itself has made its own contribution to the currency troubles in Thailand and Malaysia. These countries simply cannot fight inflation, a declining economy, a falling currency, and failing politics at the same time. Political turmoil must be addressed first, before economic and currency problems can be addressed with serious purpose.

This is a good time for currency investors to reassess where they want to be standing over the coming months. The urgency behind this need to reassess is in the nature of the currency market itself. To put it simply, the carry trade gets carried away with itself. It pours too much money into too few economies with too little ability to handle the hot inflows.

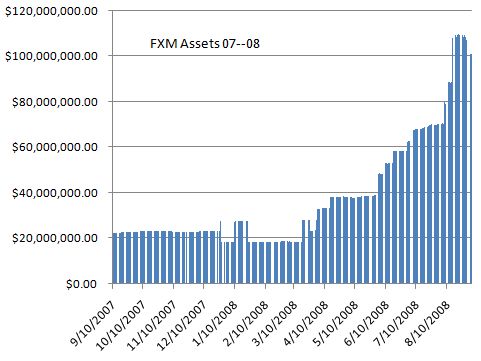

The chart below shows how the Mexican peso ETF (FXM), grew from September of last year to this month. Note the huge surge in assets under management that began around April, ’08. Mexico began raising the interest rates to suppress inflation, and the carry trader responded in a typical fashion by flooding Mexico with dollar purchases of the peso to take advantage of the higher rates.

There is no telling if this is the beginning, end, or middle of the hot money cycle for Mexico. A recent speech made by their finance minister hinted that inflation was less of a threat than it had been, thus calling into question the almost certain anticipation of continued rate increases by the Mexican central bank. The peso dropped over 1% by the end of the day.

This episode should reinforce your desire not to be long on pesos the day the U.S. Federal Reserve announces a rate increase. The mountain you see in the chart above will find it way back across the Rio Grande faster than it came south, carrying the remnants of your profits with it.

However, the events of August do not necessarily mean that the end has arrived. August is just one month. The encouraging part of this news is that while the emerging markets are taking a short term hit, there is good reason to expect them to recover without the trauma that has characterized past currency collapses. The example of Mexico bringing inflation down is a good example.

Another reason for my optimism is that the recent EM expansion was accomplished in a relatively healthy way rather than an unhealthy one. The economies of all the prime movers in the EM world are well positioned with actual production capacity, rather than the promise of capacity that exemplified past hot money expansions. At the start of the last upswing, their currencies were reasonably valued, their domestic budges were healthy, and their political systems were stable. In the 1997—99 crash, none of these descriptions would have been accurate. There was more hype and less reality behind the emerging markets boom then.

It’s also possible that the current level of inflation will moderate. There are signs other than in Mexico that high interest rates are slowing things down. If this holds, the end will come with a whisper rather than a crash, as cash balances are shifted in a convergent and orderly way.

In the meantime, I am not panicking. My carry trade holdings are intact. This may, of course, prove to be a big mistake. I may be wrong and the entire carry trade will unwind tomorrow. But, I’m taking my chances. The only recent change in my currency portfolio is the addition of UUP, the dollar bullish ETF from PowerShares. This is a way of partially hedging my bets.

If any action is called for, it is to be vigilant in following developments in the international sphere. An old saying in the currency trading community is that the carry trade is like picking up pennies in front of a steam roller. You want to keep a keen eye on the guy at the controls as well as the pennies.

*I put the PowerShares DB US Dollar Bullish Fund ETF (UUP) in the chart to show that part of the decline was due to the relative strength of the U.S. dollar.

There are two primary reasons for the battering these currencies took in August: economic slowdowns in America and Europe, and global inflation.

The slowdown in the developed economies affects emerging markets because they depend so much on exports. Investors fear it will get worse; if demand for finished products or commodities falls even a little, export-dependent economies will be hurt a lot. This describes most emerging markets today and accounts for much of the recent fall in the value of their currencies.

Unfortunately, the EM world has more than slowing demand to deal with. At the same time, that demand for their products is leveling off or falling, the tremendous growth in exports over the last few years has pushed wages and local prices up. This reaction has two unsettling effects: it encourages increased spending within the local economies, putting upward pressure on domestic prices, and it encourages businesses to raise prices to cover the higher labor costs. Combine these two factors with the increase in commodity prices that has spiked world-wide over the last few years, and you get a triple whammy of inflationary pressures.

The final result of this rather long chain of events is a tendency for local economies to raise interest rates in order to relieve inflationary pressure and ease the devaluation of their currency. Not every country does it this way, but, as you can see from the first table, many do.

Political instability itself has made its own contribution to the currency troubles in Thailand and Malaysia. These countries simply cannot fight inflation, a declining economy, a falling currency, and failing politics at the same time. Political turmoil must be addressed first, before economic and currency problems can be addressed with serious purpose.

This is a good time for currency investors to reassess where they want to be standing over the coming months. The urgency behind this need to reassess is in the nature of the currency market itself. To put it simply, the carry trade gets carried away with itself. It pours too much money into too few economies with too little ability to handle the hot inflows.

The chart below shows how the Mexican peso ETF (FXM), grew from September of last year to this month. Note the huge surge in assets under management that began around April, ’08. Mexico began raising the interest rates to suppress inflation, and the carry trader responded in a typical fashion by flooding Mexico with dollar purchases of the peso to take advantage of the higher rates.

{kind=link}

There is no telling if this is the beginning, end, or middle of the hot money cycle for Mexico. A recent speech made by their finance minister hinted that inflation was less of a threat than it had been, thus calling into question the almost certain anticipation of continued rate increases by the Mexican central bank. The peso dropped over 1% by the end of the day.

This episode should reinforce your desire not to be long on pesos the day the U.S. Federal Reserve announces a rate increase. The mountain you see in the chart above will find it way back across the Rio Grande faster than it came south, carrying the remnants of your profits with it.

However, the events of August do not necessarily mean that the end has arrived. August is just one month. The encouraging part of this news is that while the emerging markets are taking a short term hit, there is good reason to expect them to recover without the trauma that has characterized past currency collapses. The example of Mexico bringing inflation down is a good example.

Another reason for my optimism is that the recent EM expansion was accomplished in a relatively healthy way rather than an unhealthy one. The economies of all the prime movers in the EM world are well positioned with actual production capacity, rather than the promise of capacity that exemplified past hot money expansions. At the start of the last upswing, their currencies were reasonably valued, their domestic budges were healthy, and their political systems were stable. In the 1997—99 crash, none of these descriptions would have been accurate. There was more hype and less reality behind the emerging markets boom then.

It’s also possible that the current level of inflation will moderate. There are signs other than in Mexico that high interest rates are slowing things down. If this holds, the end will come with a whisper rather than a crash, as cash balances are shifted in a convergent and orderly way.

In the meantime, I am not panicking. My carry trade holdings are intact. This may, of course, prove to be a big mistake. I may be wrong and the entire carry trade will unwind tomorrow. But, I’m taking my chances. The only recent change in my currency portfolio is the addition of UUP, the dollar bullish ETF from PowerShares. This is a way of partially hedging my bets.

If any action is called for, it is to be vigilant in following developments in the international sphere. An old saying in the currency trading community is that the carry trade is like picking up pennies in front of a steam roller. You want to keep a keen eye on the guy at the controls as well as the pennies.

Subscribe to:

Comments (Atom)