August has been hard on emerging market currencies. Note the table below to see how much the currencies of some of the emerging markets fell last month.

*I put the PowerShares DB US Dollar Bullish Fund ETF (UUP) in the chart to show that part of the decline was due to the relative strength of the U.S. dollar.

There are two primary reasons for the battering these currencies took in August: economic slowdowns in America and Europe, and global inflation.

The slowdown in the developed economies affects emerging markets because they depend so much on exports. Investors fear it will get worse; if demand for finished products or commodities falls even a little, export-dependent economies will be hurt a lot. This describes most emerging markets today and accounts for much of the recent fall in the value of their currencies.

Unfortunately, the EM world has more than slowing demand to deal with. At the same time, that demand for their products is leveling off or falling, the tremendous growth in exports over the last few years has pushed wages and local prices up. This reaction has two unsettling effects: it encourages increased spending within the local economies, putting upward pressure on domestic prices, and it encourages businesses to raise prices to cover the higher labor costs. Combine these two factors with the increase in commodity prices that has spiked world-wide over the last few years, and you get a triple whammy of inflationary pressures.

The final result of this rather long chain of events is a tendency for local economies to raise interest rates in order to relieve inflationary pressure and ease the devaluation of their currency. Not every country does it this way, but, as you can see from the first table, many do.

Political instability itself has made its own contribution to the currency troubles in Thailand and Malaysia. These countries simply cannot fight inflation, a declining economy, a falling currency, and failing politics at the same time. Political turmoil must be addressed first, before economic and currency problems can be addressed with serious purpose.

This is a good time for currency investors to reassess where they want to be standing over the coming months. The urgency behind this need to reassess is in the nature of the currency market itself. To put it simply, the carry trade gets carried away with itself. It pours too much money into too few economies with too little ability to handle the hot inflows.

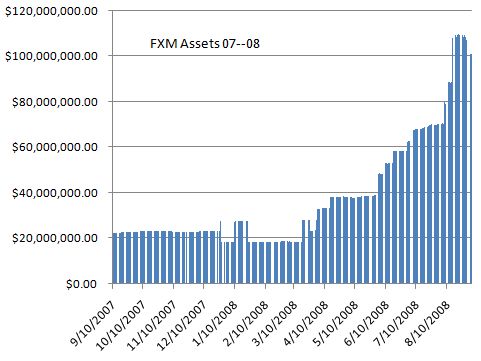

The chart below shows how the Mexican peso ETF (FXM), grew from September of last year to this month. Note the huge surge in assets under management that began around April, ’08. Mexico began raising the interest rates to suppress inflation, and the carry trader responded in a typical fashion by flooding Mexico with dollar purchases of the peso to take advantage of the higher rates.

There is no telling if this is the beginning, end, or middle of the hot money cycle for Mexico. A recent speech made by their finance minister hinted that inflation was less of a threat than it had been, thus calling into question the almost certain anticipation of continued rate increases by the Mexican central bank. The peso dropped over 1% by the end of the day.

This episode should reinforce your desire not to be long on pesos the day the U.S. Federal Reserve announces a rate increase. The mountain you see in the chart above will find it way back across the Rio Grande faster than it came south, carrying the remnants of your profits with it.

However, the events of August do not necessarily mean that the end has arrived. August is just one month. The encouraging part of this news is that while the emerging markets are taking a short term hit, there is good reason to expect them to recover without the trauma that has characterized past currency collapses. The example of Mexico bringing inflation down is a good example.

Another reason for my optimism is that the recent EM expansion was accomplished in a relatively healthy way rather than an unhealthy one. The economies of all the prime movers in the EM world are well positioned with actual production capacity, rather than the promise of capacity that exemplified past hot money expansions. At the start of the last upswing, their currencies were reasonably valued, their domestic budges were healthy, and their political systems were stable. In the 1997—99 crash, none of these descriptions would have been accurate. There was more hype and less reality behind the emerging markets boom then.

It’s also possible that the current level of inflation will moderate. There are signs other than in Mexico that high interest rates are slowing things down. If this holds, the end will come with a whisper rather than a crash, as cash balances are shifted in a convergent and orderly way.

In the meantime, I am not panicking. My carry trade holdings are intact. This may, of course, prove to be a big mistake. I may be wrong and the entire carry trade will unwind tomorrow. But, I’m taking my chances. The only recent change in my currency portfolio is the addition of UUP, the dollar bullish ETF from PowerShares. This is a way of partially hedging my bets.

If any action is called for, it is to be vigilant in following developments in the international sphere. An old saying in the currency trading community is that the carry trade is like picking up pennies in front of a steam roller. You want to keep a keen eye on the guy at the controls as well as the pennies.

{kind=link}

No comments:

Post a Comment